MARKET PULSE | Q1 2026

Early 2026 does not feel like a market rushing back into exuberance. It feels like a country absorbing external pressure without falling apart, and a residential sector that is increasingly shaped by domestic demand, infrastructure-led expansion, and housing products that people can actually use.

This article focuses on the Economic Overview and Residential Market Pulse sections of the APS Q1 2026 report, covering Cambodia’s macro conditions and residential property dynamics as of early 2026.

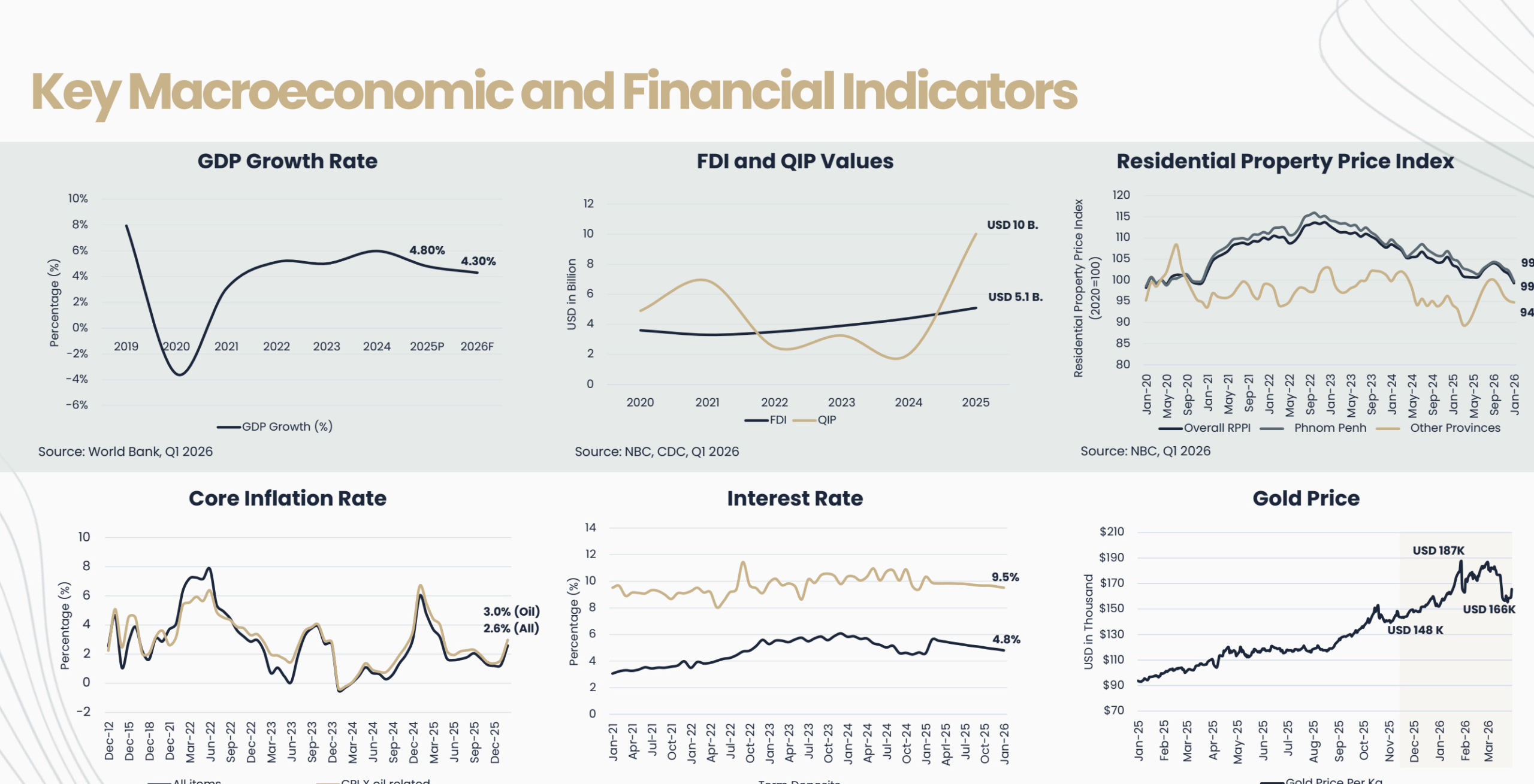

GDP Growth Forecast

4.3%

Cambodia growth outlook for 2026 (World Bank forecast).

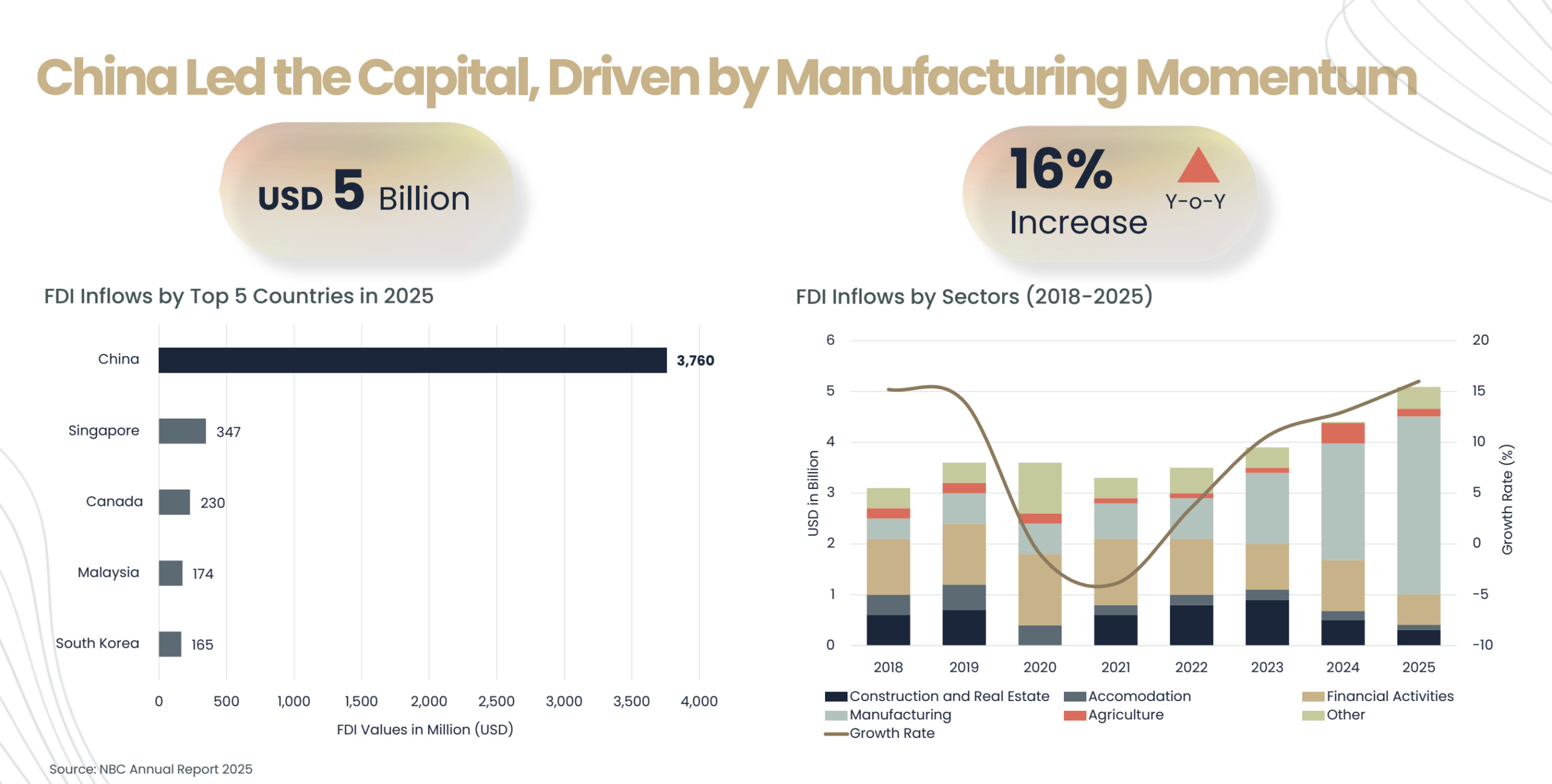

FDI in 2025

USD 5.1B

Capital inflows rose alongside stronger QIP values and manufacturing momentum.

Condo Supply

76,000+

Units across 150+ Phnom Penh condominium projects as of Q1 2026.

Landed Supply

181,000+

Units across 500+ landed property projects as of Q1 2026.

Section 1 — Economic Overview

The macro picture is steady on the surface and careful underneath. Growth, inflation, and property indicators are not signalling panic, but the operating environment still rewards patience.

Resilience is visible, but confidence is still guarded

The first quarter of 2026 looks like a period of resilience under pressure. Energy shocks, geopolitical tension, and a more unpredictable financial climate have made investors more defensive, not more adventurous. Predictability is scarce, and that alone is enough to keep decision-making conservative.

Even so, the dashboard does not read like a market in retreat. Growth is still expected to hold, with a World Bank forecast of roughly 4.3% for 2026. Inflation appears more contained than destabilizing, and the residential property price index looks soft rather than distressed. Interest-rate conditions still suggest caution in the banking system, but not paralysis.

That combination matters. Cambodia is not racing ahead on easy money. It is absorbing pressure while maintaining enough stability to keep property activity moving, especially where demand is grounded in actual use rather than speculation.

The most important economic signal here is not acceleration. It is endurance. Stability itself has become a competitive advantage in a noisy regional backdrop.

Macro Takeaway

Capital is still flowing, but the story is concentrated

One of the clearer positives in the market is capital formation. The chart set shows FDI at about USD 5.1 billion in 2025, while QIP values rise much faster and point to a stronger pipeline of approved activity. The data also shows a 16% year-on-year increase in inflows, with China far ahead of the rest of the field at roughly USD 3.76 billion.

This is not portrayed as broad-based enthusiasm across every sector. It is more targeted than that, and the manufacturing story does a lot of the work. For real estate, that nuance matters: stronger capital inflows can help sentiment, employment, and industrial momentum without automatically reviving every property segment at the same speed.

When inflows are led by manufacturing and productive sectors, the knock-on effect is usually more gradual and more structural. That tends to support real housing demand better than a short-lived speculative wave.

Why This Matters for Property

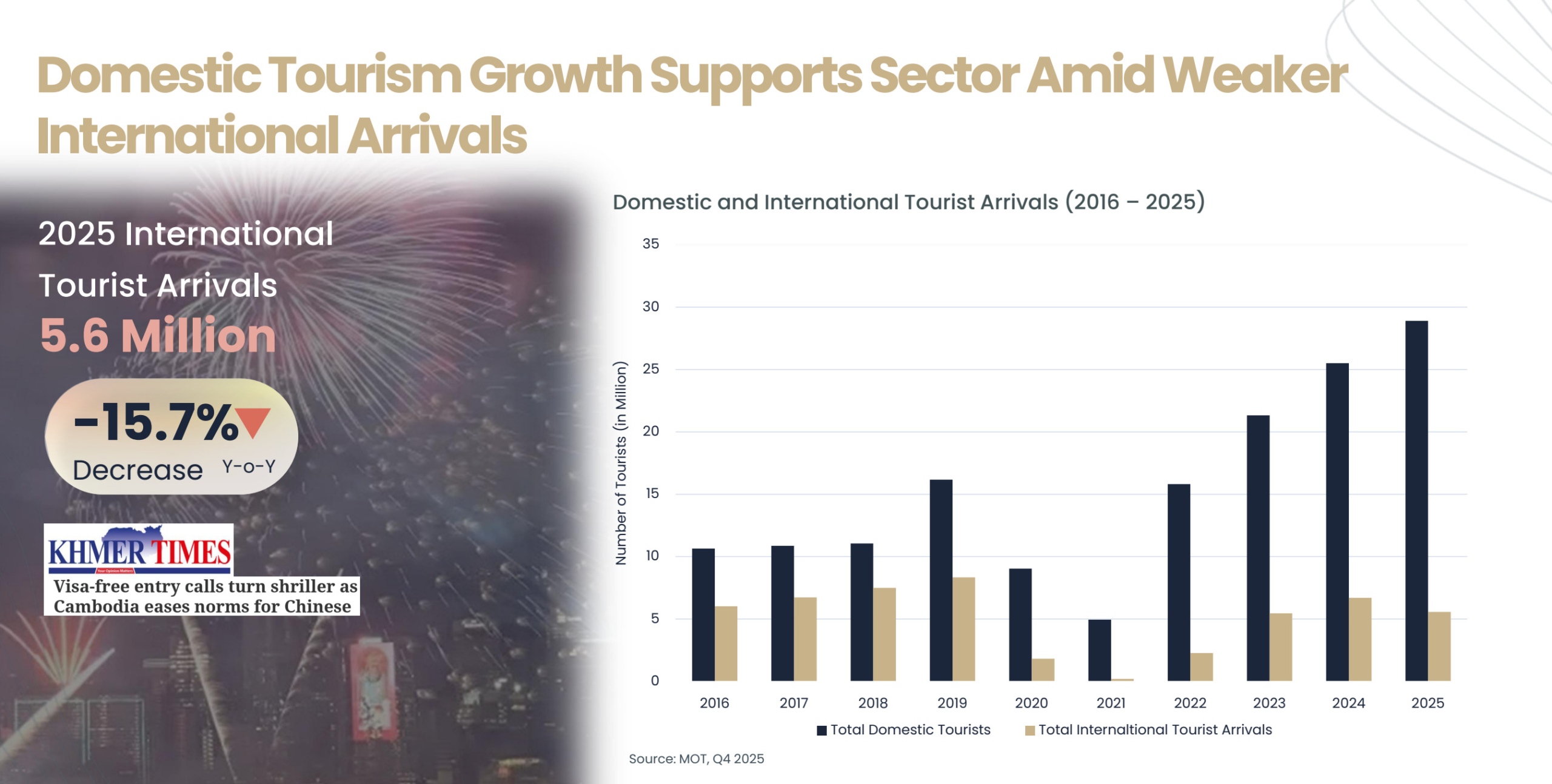

Tourism still supports the economy, but the rebound is uneven

Tourism remains a softer pillar than many investors hoped. 2025 international tourist arrivals came in at 5.6 million, down 15.7% year on year. That is a meaningful reminder that Cambodia is still exposed to weaker external travel patterns and tighter household budgets abroad.

Domestic tourism is doing more of the stabilizing work, helping keep activity levels from falling as sharply as international numbers alone might imply. For property, this means hospitality-linked confidence can improve, but likely in a measured, selective way rather than through a broad demand surge.

Tourism is still an economic pillar, but it is no longer a clean rebound narrative. Cambodia is advancing through mixed support rather than one dominant growth engine.

The Wider Reading

Section 2 — Residential Market Pulse

Residential market movement becomes most visible here. Demand has not disappeared. It has shifted toward local users, more realistic pricing, and corridors where infrastructure can still translate into long-term value.

Condominiums are being pulled back toward real demand

Condominium market activity is increasingly organised around what buyers can absorb. As of Q1 2026, Phnom Penh condo supply sits above 76,000 units across 150+ projects, with mid-range stock holding 61% of supply, affordable products at 26%, and high-end projects at 13%.

Developers are no longer designing primarily for the old buy-to-invest narrative. They are pushing more product into the buy-to-use segment, where local households and younger buyers are more open to vertical living than in earlier cycles. That is why mid-range still anchors the market, while affordable supply is growing into a much more meaningful share of future launches.

The upper end is not gone forever. High-end launches have started to reappear, but only as a secondary theme. The centre of gravity remains firmly in the practical segments where sales absorption still justifies completion.

This is less a luxury comeback story than a demand reset. Developers appear to have accepted that volume now comes from affordability, usability, and a better fit with domestic purchasing power.

Condo Read-Through

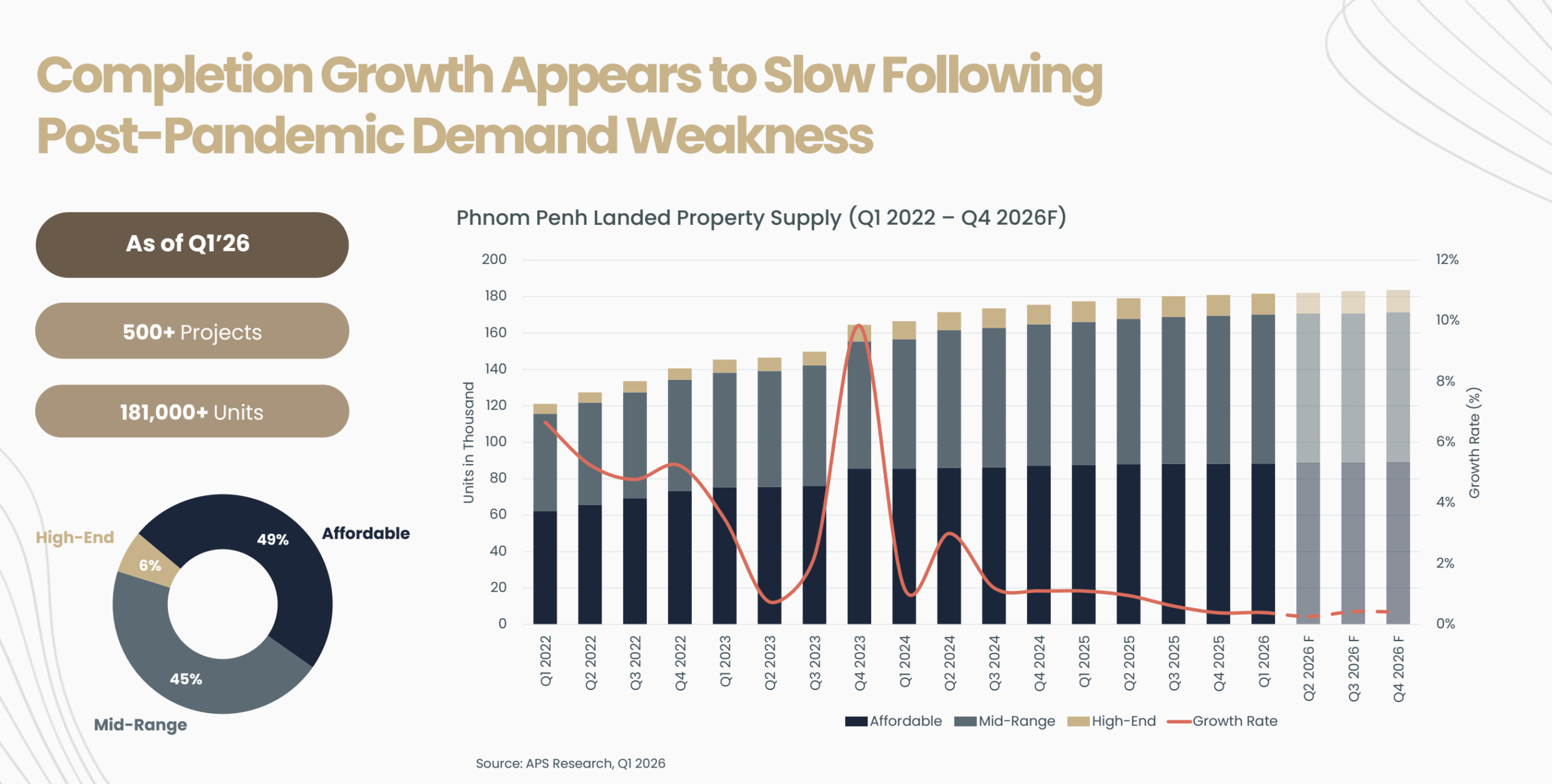

Landed property still holds the strongest cultural and commercial pull

If condominiums are becoming more acceptable, landed homes remain the instinctive first choice for many Cambodian buyers. As of Q1 2026, Phnom Penh’s landed property stock exceeds 181,000 units across 500+ projects, and the market is almost evenly split between affordable (49%) and mid-range (45%) product. High-end landed supply remains a niche player at just 6%.

The more important story is geographic. New launches and completions are increasingly clustering in the south, where lower land costs still allow developers to keep pricing within reach and where major infrastructure — especially the airport corridor and access roads — is creating a credible expansion path.

This corridor follows a familiar urban sequence: residential comes first, then commercial uses follow once population density and traffic flow are established. In other words, the southward shift is not just about cheaper land. It is about where developers and buyers still see future capital appreciation.

Infrastructure matters less as backdrop and more as pricing logic. In this part of the market, proximity to new roads and major nodes is still being read as value creation, not simply as urban inconvenience.

Why the South Matters

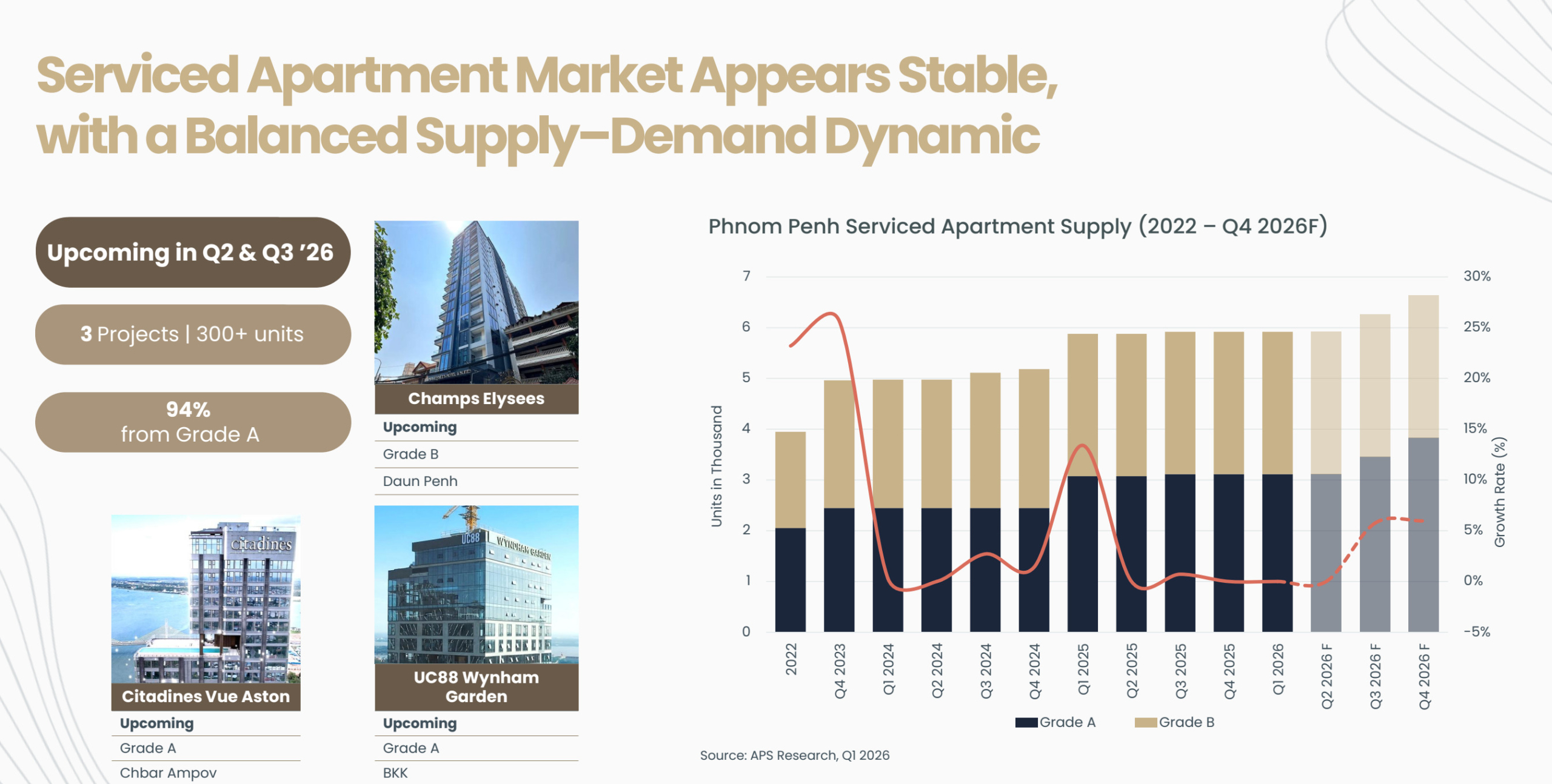

Serviced apartments look more balanced than overheated

Among the three residential subsectors, serviced apartments look the healthiest in terms of supply-demand balance. The pipeline is measured rather than excessive, and that matters in a city where newer residential stock can quickly compete for the same tenants.

The near-term pipeline includes 300+ upcoming units across three projects in Q2 and Q3 2026, with 94% of that pipeline in Grade A. Branded operators and upcoming openings point to confidence, but not to oversupply. The distinction matters: momentum exists here precisely because the segment has remained disciplined.

That makes serviced apartments a useful contrast to older boom-cycle assumptions. Stability, measured additions, and a clear target tenant base now matter more than chasing aggressive expansion.

A sudden breakout is not the most convincing reading here. The healthier view is that the market has stayed tight enough to avoid a damaging oversupply cycle, which is a strength in itself.

Balanced, Not Booming

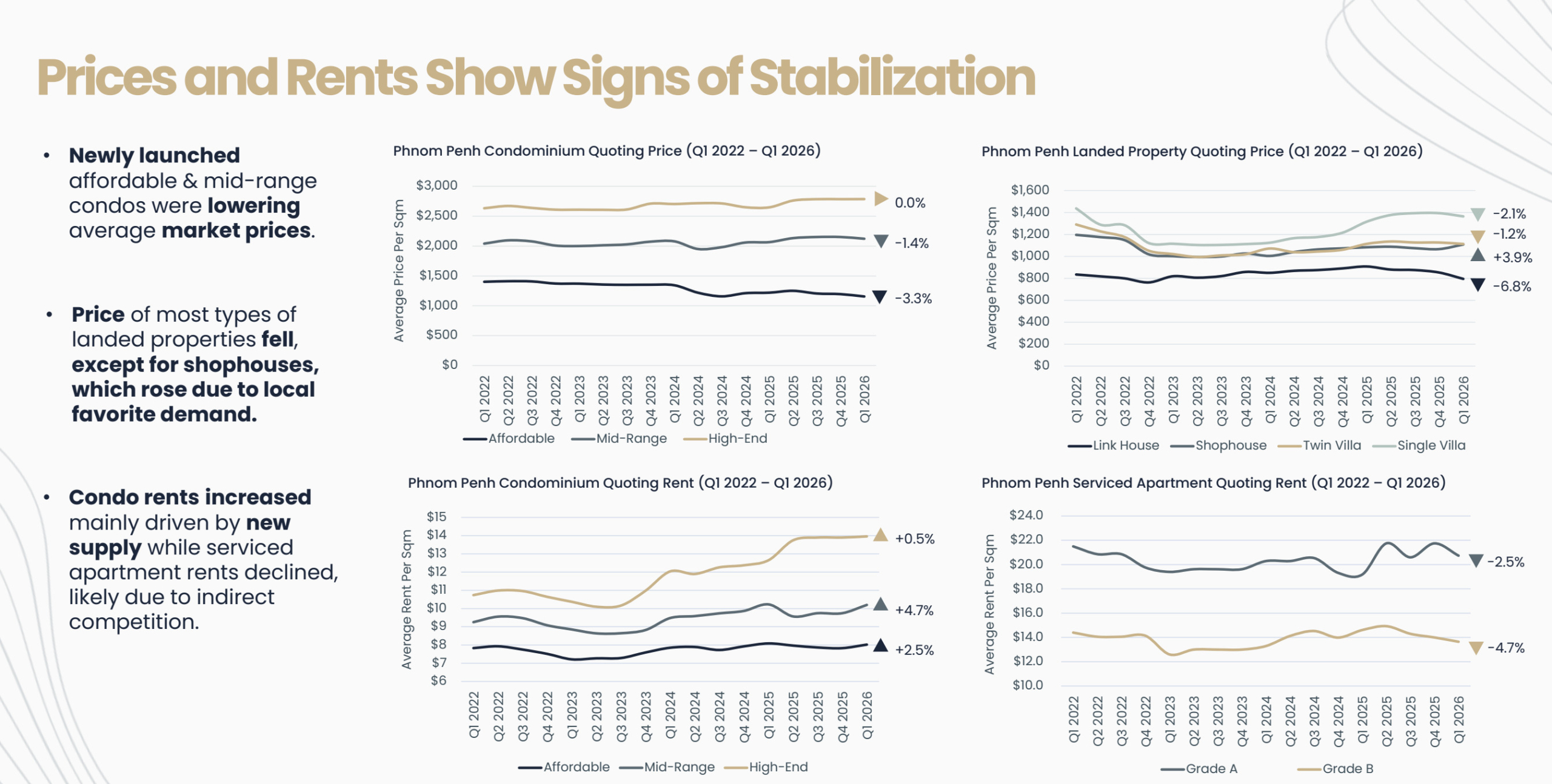

Prices and rents are starting to behave more normally

The final residential chart is arguably the most reassuring one in the set. Prices and rents are showing signs of stabilization. That does not mean every line is turning upward, and it does not mean all segments are equally strong. It means the market is moving away from sharp swings and back toward something more rational.

Affordable and mid-range condo launches have been pulling average condo selling prices lower, which is consistent with the market’s shift toward more attainable stock. In landed property, most product types have softened, but shophouses stand out as an exception because local demand still supports them. On the leasing side, average condo rents have edged up as newer product enters the market, while serviced apartment rents have slipped under the pressure of indirect competition from condominiums.

This is a healthier market signal than it may sound. Stabilization means developers and occupiers are beginning to operate inside a more believable price environment, and that is exactly the kind of base from which more durable recovery usually starts.

Stability is not glamorous, but it is investable. Phnom Penh housing is moving toward a phase where pricing is being shaped by real user demand rather than headline optimism.

The Practical Conclusion

A quieter market can still be a stronger one

Taken together, the two sections tell a consistent story. Cambodia’s macro environment is still carrying risk, but it is not breaking. At the same time, Phnom Penh’s residential market is becoming less dependent on speculative narratives and more dependent on domestic affordability, usable product, and infrastructure corridors that can support everyday life. That may feel less dramatic than the boom years, but it is also a more believable foundation for the next phase of growth.

Source: APS Research Q1 2026 market report. Scope intentionally limited to the Economic Overview and Residential Market Pulse sections.

Source Video:

Ta strona jest także dostępna w językach:

![]() Polski (Polish)

Polski (Polish)