The residential market in Phnom Penh has been experiencing a gradual shift throughout 2024, with slower project completions and a mixed trend in property prices. This slowdown is evident across various sectors, including condominiums, landed properties, and serviced apartments. However, strategic pricing and demand responsiveness in specific segments suggest opportunities for developers and investors willing to adapt to the evolving market landscape.

Condominium Market: Mixed Trends in Pricing

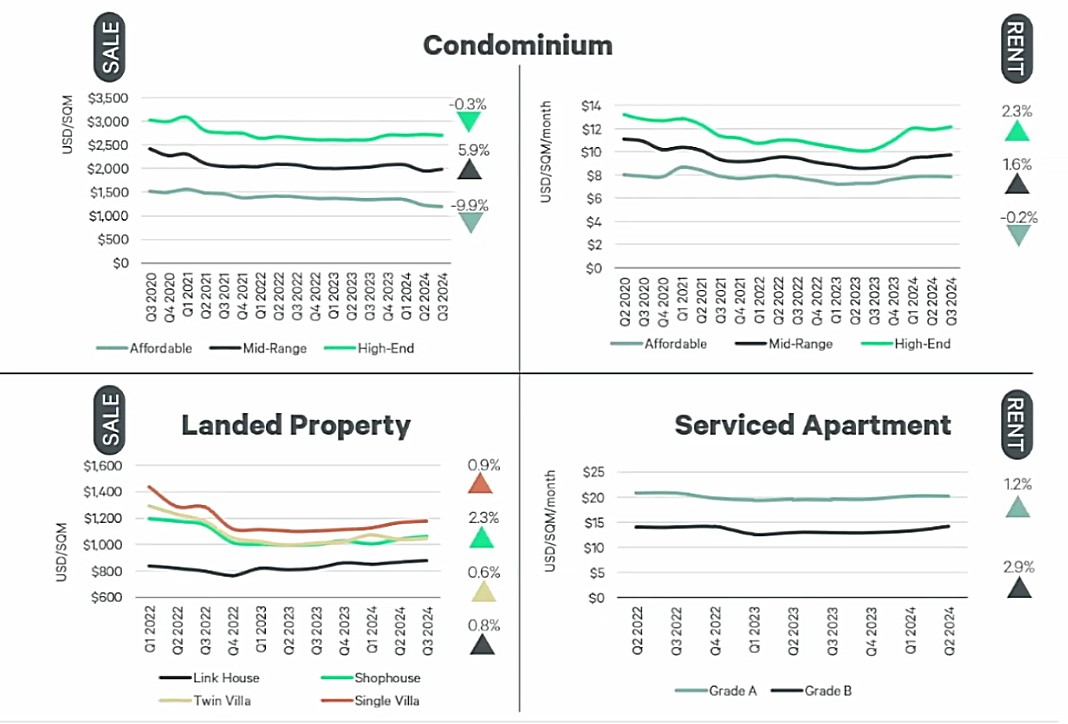

In Q3 2024, the condominium market witnessed divergent price trends across different segments:

- Affordable Condominiums saw a significant price decrease of 9.9%.

- Mid-Range Condominiums, on the other hand, experienced a 5.9% price increase, driven by new project launches.

- High-End Condominiums had only a slight decline of 0.3%, reflecting relative stability in this sector.

The rental market for condominiums painted a different picture, with rent prices showing minor yet positive adjustments:

- Affordable Condominiums saw a modest decrease of 0.2% in rent.

- Mid-Range Condominiums rents increased by 1.6%.

- High-End Condominiums experienced a more pronounced rent increase of 2.3%.

The rise in mid-range properties indicates a growing demand for units that strike a balance between affordability and quality. New launches in this segment have performed well, with pricing playing a critical role in attracting buyers despite overall market caution.

Landed Property Market: Steady Growth with Focus on Shophouses

Landed properties in Phnom Penh continued to grow, although at a modest pace:

- Houses increased by 0.9% in sale prices.

- Shophouses, the most dynamic in this category, saw a price rise of 2.3%, highlighting strong demand for mixed-use properties.

- Twin Villas and Single Villas experienced minor increases of 0.6% and 0.8%, respectively.

Despite the slower completion rates, landed properties remain a preferred choice for local investors, especially shophouses, which benefit from both residential and commercial use cases. The steady price growth in these categories suggests resilience even amidst economic uncertainties.

Serviced Apartments: Rising Demand for Grade B Units

The serviced apartment sector also reflected a trend of steady growth, particularly in rental prices:

- Grade A apartments saw a 1.2% increase in rents.

- Grade B apartments outperformed with a 2.9% increase, indicating strong demand for mid-tier serviced living options.

This trend suggests that while the high-end market remains stable, there is a growing preference for more affordable luxury in serviced apartments, particularly from expatriates and professionals seeking value in Phnom Penh’s competitive rental market.

Key Trends and Market Adjustments

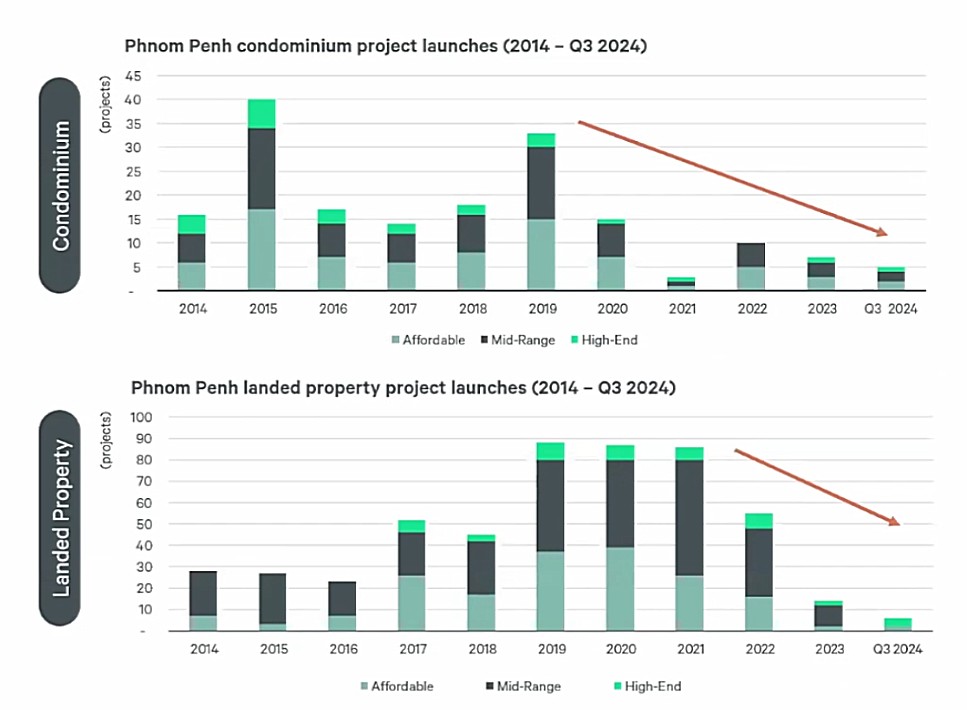

The Phnom Penh residential market is in a period of recalibration, marked by fewer new project launches and slower completion rates. This moderation follows years of rapid expansion, especially before the COVID-19 pandemic. For example, new condominium launches have plummeted since 2020, with fewer than 10 new projects per year from 2021 to 2024. Landed property projects also dropped sharply, with fewer than 20 new projects expected this year.

While this slowdown might seem concerning, it presents a healthier balance between supply and demand. The reduced supply growth is allowing demand to catch up, potentially helping to absorb the excess inventory accumulated in recent years.

At the same time, developers have become more strategic with pricing. Mid-range condominium projects, in particular, have seen success due to their competitive pricing strategies. With many projects offering prices below $1,500 per square meter, developers are targeting price-sensitive buyers, helping to drive demand even in a cooling market.

External Factors Supporting the Market

Several external factors are also supporting Phnom Penh’s residential market. Tax incentives such as the stamp duty exemption for houses priced under $70,000 have provided relief to buyers in the affordable segment. Additionally, lower interest rates offered by major developers are helping to ease financing costs for buyers. For instance, a typical developer loan interest rate has dropped from 12% to 9% per year, with loan tenures extending from 15 to over 20 years. These measures are expected to stimulate transaction volumes in the coming quarters.

Conclusion: A Market in Transition

Phnom Penh’s residential market in 2024 reflects both challenges and opportunities. While project launches and completions have slowed, strategic pricing, demand responsiveness, and supportive government policies are helping to stabilize the market. Developers who position their projects with the right pricing and long-term incentives will likely continue to find buyers, especially in the mid-range condominium and landed property sectors. As the market rebalances, investors who remain flexible and adaptive will find attractive opportunities in the city’s evolving residential landscape.

based on CBRE Cambodia Q3 2024 Market Insight

Ta strona jest także dostępna w językach:

![]() Polski (Polish)

Polski (Polish)